On the 17th of January 2023, I attended the AGM of Frasers Logistics & Commercial Trust (FLCT) at Intercontinental Hotel Singapore. These are some interesting/important points brought up during the AGM. An early disclaimer. My note-taking skill has become rusty compared to my college days, so please pardon some missing details. This is more like a paraphrased summary :)

The CEO’s Presentation:

Rental growth rate in the UK, Germany & Dutch markets

are CPI-linked. So given the higher inflation currently seen in Europe, FLCT

should be poised to enjoy positive rental reversions in 2023.

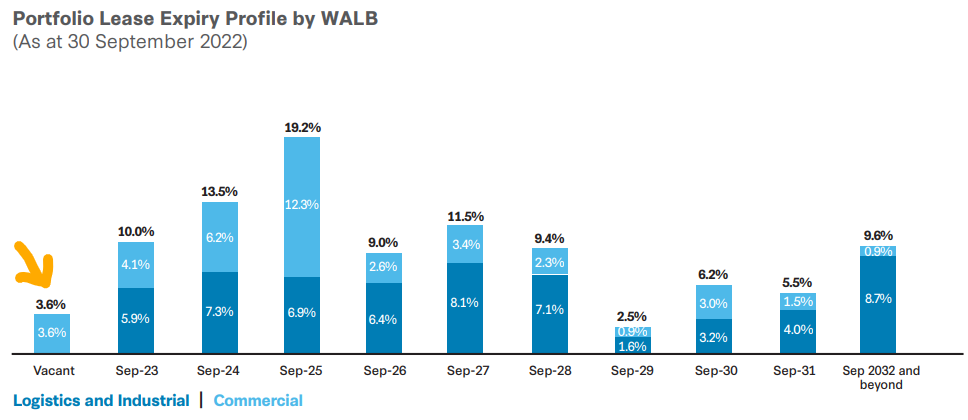

Management is in advanced negotiations to lease the

remaining vacant space in 2023. Only very little space left. Lease expiry profile

remains strong. No more than 19.2% of GRI expires in any given year until 2032.

Most of FLCT’s energy costs is passed on through to

tenants.

FLCT has one of the lowest gearing ratio in the S-REITs

sector at 27.4%. A healthy aggregate leverage should help to tide it over the current

higher rate environment.

Q & A Session with Unitholders:

Question: What is the strategic direction of FLCT? Will

commercial assets be sold to buy more logistics/industrial (L&I) assets?

CEO answers: The sale value of Cross Street Exchange building

was just too attractive. The property was not sold because it was underperforming.

Moving forward, FLCT aims to have a slightly higher allocation to L&I sector.

Not looking to buy more commercial properties. Still satisfied with the current

rental yield, rental growth and occupancy of commercial assets in FLCT’s

portfolio.

Question: Looking at the debt maturity profile, there is sizable

refinancing needs in 2024 in the Euro currency. Is it a concern having a huge

amount of Euro-denominated debt?

CFO answers: FLCT already has facilities in place to

refinance the debts in 2023. Management is currently focusing on refinancing

for 2024. Would have some impact on distributable income. The latest interest

rate sensitivity check is for every 50bps rise in interest rate, the DPU will

be down 0.05 cents approximately. The management already hedged 82% of debts to

fixed rates, so only the debt on floating rates will be affected. Natural hedging

is also done by borrowing in the currencies of those countries where

acquisitions are made. Euro-denominated debts is not in excess of FLCT’s

portfolio asset value in Europe. There is no over-weightage of debt in any

single currency.

Question: Is there danger of further rise in the cap rate?

CEO answers: Cost of debt and rental income growth

expectations affect the cap rate. For commercial assets, there is no income expectation

function in the market. His gut feel is that there will be no more significant

rise in cap rate. FLCT has ‘taken the medicine’ so as to speak.

Question: What is FLCT’s geographical focus for future

growth? What are the characteristics the management look for when they do acquisitions?

CEO answers: Comfortable in the current geographical allocation. Difficult to expand into new markets because of higher interest rates. Like to partner with the sponsor on development projects as they have people on the ground, staff that can speak German or Dutch and have local knowledge/connections. Continue to mainly grow L&I assets a little more, supported by commercial assets. But never say never, if a compelling deal comes up on their radar, FLCT is ready to take action since it has a healthy gearing ratio. Acquisitions must be DPU-accretive. But such deals are tough to find in current market conditions.

Question: Concerns about the lower occupancy rate at some

UK properties namely Farnborough Business Park and Blythe Valley Business Park.

CEO answers: Seeing the tenants either looking to take up

less space or going for better quality space. There is a flight to quality. The

pandemic era work-from-home trend is starting to reverse as companies tell their

employees to return to the office for more days. This is his personal opinion. Due

to economic uncertainties, the labour market is becoming an employer market

where companies have more say and make more demands from employees. Hopefully,

this trend continues.

Question: FLCT has over S$217m in divestment capital gains. How is management planning to use this?

CEO answers: It could be used to mitigate the loss of income from the sale of Cross Street Exchange. But FLCT has to borrow/take on debt in order to distribute these capital gains to unitholders.

CFO answers: The impact of forex on DPU would be AUD down

3%, Euro down 7% and British Pound down 5% on average.

Question: Is there a final target for the gearing ratio?

CEO answers: The current gearing ratio of 27.4% is a nice

place to be in for now, due to higher interest rates. But eventually, the

target is mid-30s once interest rates and cap rates normalise in the future.

Question: Can the management give their take on the impact of Ukraine-Russia conflict on FLCT’s operations?

CEO answers: FLCT’s European portfolio remains resilient

despite the war. Occupancy rates remain high. Tenants are sourcing supplies

from outside of Ukraine. Do not foresee any huge impact on L&I leasing

demands.

Question: What is the capital allocation for future

acquisitions?

CEO answers: We are still in a rising rate environment and

a price-resetting phase in the property market. FLCT wants to buy DPU-accretive

assets but we must be patient and selective. When a great opportunity comes

along, FLCT is ready to execute.

Question: Many S-REITs, not only FLCT is facing the twin headwinds of rising interest rates and forex risks. Some investors are even switching their funds to fixed income instruments. Can the management provide some reassurances to allay unitholders fears?

CEO answers: On the challenge of higher rates, FLCT can try to control its gearing ratio and hedging the debts to fixed rate. But honestly, we are at the mercy of the US Federal Reserve because the entire world follows them. No amount of mitigation measures can fully shield FLCT from the impact of rate hikes. Forex risks would be harder to mitigate due to its volatility and unpredictability. Can only do hedging to lower the risk.

Chairman answers: We can sit here all day discussing about

interest rates and macro-economic issues, but even the Central Bankers who are

supposed to know what they are doing, are confused too. The best thing we can

do is to stay in countries that have proven to manage economies well throughout

many economic cycles.

Question: Does FLCT own any treasury units?

CFO: No, FLCT does not own any treasury units.

A sumptuous buffet was provided after the AGM ended. The space is a little cramped though.