Total Cumulative Dividends (2010 - 2025): S$371, 015

Current Cash & Cash Equivalents: S$23, 000

(*All figures are accurate as of 31 Dec 2025)

Portfolio Actions in 4Q 2025:

Subscribed to Keppel DC REIT preferential offering

Accumulated PropNex at S$1.87

Accumulated Amazon at US$221

Accumulated Alphabet at US$298 and US$306

Accumulated Microsoft at US$477

Accumulated Nvidia at US$179

Multi-Year Heavy Bets Paid Off Handsomely

2025 was a great year in terms of investment returns. All the counters in my portfolio ended the year in the green except three losers. My top five winners in 2025 (excluding dividends) were PropNex (+102%), Alphabet (+66%), Sheng Siong (+59%), DBS (+29%) and CapitaLand Integrated Commercial Trust (+21%). My bottom three losers (excluding dividends) were Mapletree Industrial Trust (-9%), UOB (-4%) and Keppel DC REIT (flat). In terms of total dividend payout, a record-high of $46k was achieved largely thanks to hefty special dividends from the three local banks and PropNex.

My thesis on Sheng Siong and PropNex finally paid off big in 2025. I built up significant positions on both counters through constant, steadfast accumulation since 2023. I even did one last aggressive buy when the Trump Tariffs correction hit in April. The massive tailwind finally arrived in May 2025 after the incumbent government clinched a strong mandate during the General Election. Both PropNex and Sheng Siong stand to benefit long-term from government policies (which I mentioned in previous posts). In the second half of the year, both counters kept breaking new highs. Although recently, PropNex had retraced back to S$1.90, it still ended up as my top performer for the year.

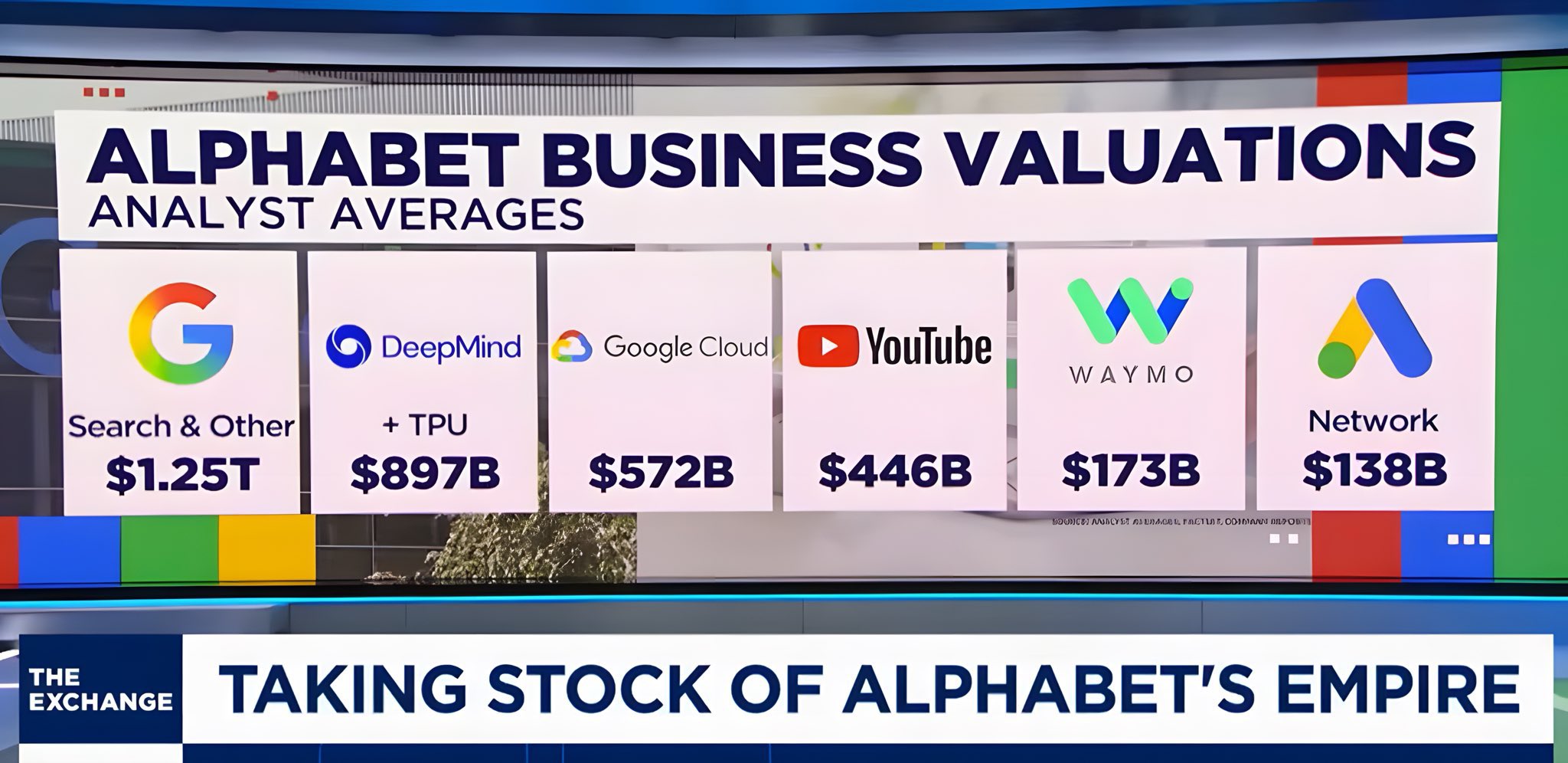

Next, my thesis on Alphabet also yielded huge returns in 2025. It is my current top US position by far. I always thought the narrative around the death of Google Search was overblown. Too much doom and gloom. Again, bought aggressively back in Q2 2025. YouTube is bigger than Netflix and still growing. Google Cloud posting robust year-on-year growth. Android OS deeply entrenched on all smartphones outside of Apple's iPhone. Waymo is expanding its robotaxi service into new markets. One of the major shareholders of SpaceX. I also bet on a favourable verdict from its anti-trust case, which did came true. The emergence of OpenAI actually helped to prove Alphabet's argument that its search business is not a monopoly because ChatGPT is a rival. In the end, the US Department of Justice did not require Alphabet to break up and sell off Chrome. So, Alphabet's eco-system moat remains intact. It owns an entire integrated AI stack. Furthermore, I am confident that Google's AI model will eventually catch up to ChatGPT and that came true too. Google Gemini 3 AI model is pretty much on par with ChatGPT 5 right now. I have started incorporating Gemini into my daily life and it works fine. Not to mention how insanely useful Google Maps and Translate proved to be during my trips to Tokyo, Osaka and Bangkok.

First-ever Trip to Osaka

My gradual transition from wealth accumulation to enjoying my fruits of labour continued with my recent trip to Osaka. Putting some of my dividends to good use. Improving my quality of life bit by bit. For now, I aim to travel to two places per year. Eventually, I plan to visit four destinations per year. Secondly, I also look to upgrade at least one thing I use regularly in my life every year. This year, I upgraded from regualr iPhone 15 to an iPhone 17 Pro. I had a great time using it to navigate, take photos and film videos on my Osaka trip.

Total Cumulative Dividends (2010 - 9M2025): S$364, 225

Current Cash & Cash Equivalents: S$17, 000

(*All figures are accurate as of 30 Sep 2025)

Portfolio Actions in 3Q 2025:

Accumulated batches of Alphabet at US$200 & US$246

Accumulated batches of Amazon at US$219 & US$222

Accumulated Microsoft at US$505

Markets Were Cooking Hard In Q3!

All of my heavy aggressive dip-buying back in the previous quarter continued to bear fruits in Q3. My 2-year strategy of accumulating positions in non-REITs counters like the banks, Sheng Siong, PropNex and US big tech has worked out pretty well so far. Even some quality S-REITs had slowly recovered as the US Fed cut rates. Just when I thought the markets could not possibly rally further, it continues to blow my mind. People who took profits earlier could not get back into the rally. I'm glad I could easily resist the temptation (patting myself on the back). As the late Charlie Munger said, 'Profits are not made in the buying or selling. It is made from the waiting.' Let your winners run. And oh boy, did my winners run! In the local market, DBS, PropNex and Sheng Siong hit new all-time-highs. In the US market, Alphabet, Microsoft & Nvidia kept breaking new highs too. Especially Alphabet, when the company received a favourable verdict from the DOJ. Google does not need to break up. All these factors pushed my portfolio value above $1 million on 29 Aug 2025. I finally entered the 7-figure club! Truly a historic moment in my investment journey.

My portfolio exceeded $1m for the first time ever on 29 Aug 2025

DBS, PropNex & Sheng Siong carried my portfolio hard

Of course, I'm under no delusion that good times never last long especially for cyclical stocks like PropNex and DBS. That is why for the first time in a long time, I stopped accumulating them at current valuations. For now, I own enough. Time to chill, collect CD and build up my warchest again. My only significant portfolio action in Q4 would probably be subscribing to Keppel DC REIT's preferential offering. KDC is using the proceeds to acquire an AI-ready hyperscale data centre in Japan. On the US market front, I managed to nibbled some Alphabet, Amazon and Microsoft in the final week of September. The current US government shut-down might give me some buying opportunities but I think investors already grown more immune to this yearly political circus.

Spending My Dividends

As the end of 2025 approaches, my work load lessens and it is time to slow down. Preparing for my first ever trip to Osaka next month. Can't wait! :)

Total Cumulative Dividends (2010 - 1H2025): S$349, 755

Current Cash & Cash Equivalents: S$3, 000

(*All figures are accurate as of 30 Jun 2025)

Portfolio Actions in 2Q 2025:

Accumulated UOB at S$30.70

Accumulated Sheng Siong at S$1.70 and S$1.83

Accumulated PropNex at S$1.03

Accumulated NetLink Trust at S$0.875

Accumulated ParkwayLife REIT at S$4.02

Subscribed to FCT's preferential offering at S$2.05

Accumulated batches of Amazon between US$170 and US$180

Accumulated batches of Alphabet between US$150 and US$160

Accumulated batches of Microsoft between US$360 and US$370

Accumulated batches of Nvidia between US$100 and US$120

TACO Man Is My God of Fortune

In April, Trump's Liberation Day tariffs threw the global markets into chaos. Doom and gloom headlines dominated the media. Youtubers were churning out daily videos with their mouth wide-opened and hands-on-forehead thumbnail images. As a battle-hardened investor, I knew this was the moment to unleash my cash warchest and dividends. My strategy of 'Sheng Siong + US tech' went into overdrive. More than S$50k deployed into the markets in Q2. I am so glad to have bought the dip aggressively because it is starting to pay off by the end of June as the US market made an incredible V-shaped recovery! My Microsoft and Nvidia positions hit all-time-high. Not even the short-lived conflict between Israel and Iran could derail the market rally despite the media touting the possibility of World War 3.

Some of my better quality REITs like AREIT, FCT, KDC and PLife have also risen YTD. Share prices of the 3 local banks remain elevated. PropNex is also riding high due to its special dividend payout and more new private property launches this year. Homebuyers have been snapping up Executive Condos (EC) like hotcakes in Q1- Q2. Sheng Siong opened 8 new outlets in 1H2025 as its share price hits an all-time-high of $1.90. More importantly in Singapore's context, the results of GE 2025 gave the incumbent party a clear and strong mandate to guide Singapore through uncertain times. Over the years, I have realised that complaining about the government policies is a waste of time. Instead, we should think of ways to gain from the system. I believe Sheng Siong, PropNex and the local banks would stand to benefit from government policies. This is a system that 65% of voters agreed upon. Let's face it, $1m resale flats is the new norm now. And judging from the URA Masterplan 2025 (Property agents already posting videos on how to become Huat Kueh), I won't be surprised to witness the first S$2m resale flat transaction in my lifetime. So just position ourselves accordingly and let the government work hard to boost our property values.

All of the above-mentioned factors combined to push my portfolio value to a new record-high of S$875k. Hefty special dividend payouts from DBS, UOB, OCBC and PropNex is set to lift my projected 2025 total dividends above S$45k. Unfortunately, on the flip side, I am expecting to run out of targets to accumulate in 2H2025 unless a new major crisis emerges. Hopefully, President Trump can cook up some crazy executive orders again. Or perhaps China can conduct some military exercises in the Taiwan Strait.

Spending My Dividends In Thailand

Visited Bangkok back in February. Enjoy good food and relaxing massage :)

Total Cumulative Dividends (2010 - 1Q2025): S$330, 984

Current Cash & Cash Equivalents (SSB/T-bills): S$26, 000

(*All figures are accurate as of 31 Mar 2025)

Portfolio Actions in 1Q 2025:

Accumulated DBS at S$44.80

Accumulated Amazon at S$183

Accumulated Alphabet at US$151

Accumulated Microsoft at US$377

In times of market turmoil, allow me to point all of you to my 'old but gold' blog post on staying unbreakable. Cultivate your inner Warrior spirit and never let a crisis go to waste!

Total Cumulative Dividends (2010 - 2024): S$324, 925

Current Cash & Cash Equivalents (SSB/T-bills): S$46, 000

(*All figures are accurate as of 31 Dec 2024)

Portfolio Actions in 4Q 2024:

Accumulated DBS at S$42

Accumulated OCBC at S$16.50

Accumulated Propnex at S$0.91

Accumulated Sheng Siong at S$1.63

Accumulated MINT at S$2.19

Accumulated Alphabet at US$188

Accumulated Nvidia at US$137

Partial divestment of KDC at S$2.23

Partial divestment of FLCT at S$0.91

A Quarter of Heavy Rebalancing - Singapore for dividends & US for growth

In 2024, REITs had been a drag on my portfolio performance, Fortunately, my positions in banks and US tech helped to mitigate some of the damage. Higher dividends from the banks was much welcomed too. In fact, the banks have rallied so much that DBS and OCBC have become my top two positions. The rebalancing of my portfolio continued with greater pace in the last quarter of 2024. The US Fed signals a slower pace of rate cuts in 2025. US core inflation remains sticky above 2% and the labour market seems resilient with the US economy booming. The era of near-zero interest rate is probably not returning anytime soon. In a normalised interest rate environment, it is better to divert my funds towards non-REIT dividend-paying counters in Singapore. Particularly, Sheng Siong for its defensiveness, Propnex and the banks for their stable growth. In an increasingly turbulent world, Singapore is a safe haven where the super rich (in Asia especially) prefer to park their wealth at. This trend should benefit the private wealth management sector and the residential property sector.

Furthermore, for the benefit of my non-local readers, you need to understand that Singaporeans (like most Asians) are obsessed with home-ownership. The idea of owning a home is deeply-ingrained into our nation's psyche, passed down through the generations. The 'Singapore Dream'. The holy grail of the middle-class. Over the past decade, home-ownership rate in Singapore has hovered around 90%, which is one of the highest in the world! Around 70% of residents live in public housing. This is why, in my opinion, the government would not launch any drastic property cooling measures as this could risk incurring the wrath of homeowners. Nobody likes to watch their property value stagnate or decline. So the government has to try to strike a fine balance between price appreciation and affordability. I guess the bottom line is, property values would be allowed to trend up in order to keep the majority of the voters happy. Over the long term, banks and Propnex should benefit from this mandate. Lastly, over the next decade, the entire Millennial generation would enter their prime home-buying and property-upgrading age. During Chinese New Year gathering last year, all my married cousins were discussing about resale HDB and condominiums launches. It was a hot topic. They are in their mid-30s to early-40s. I remember one of them was interested in a 9th-floor 5-room resale DBSS in Hougang, with an asking price of $950k. We are looking at a future where $1m HDB flats are no longer a shocker.

There was some volatility in the US market just before the US presidential election in November and I took the opportunity to buy the dip on Alphabet and Nvidia. In 2025, I am also looking to increase my allocation in Amazon and Microsoft. Most of the dividends collected from my Singapore holdings would be re-invested back into these US Big Tech. Hopefully, Mr Market can give me more buying opportunities.As for my current REIT positions, I am comfortable holding onto the more resilient ones like FCT, PLife, MINT and AREIT. But I do not plan on adding anymore. If there is a market crash, my S$40k parked in SSB would be deployed.

Preparations For FIRE Lifestyle

Going from being employed at a full-time job to a FIRE lifestyle is not as simple as flipping a switch overnight. There is a transitional period. I think we actually need time to plan and get prepared for this transition. Some people in the FIRE community are struggling at this. Throwing the resignation letter at your boss's face is the easy part. Entering a new stage of your life can be challenging. Some people start to get bored or lose their purpose in life. This is why I started my preparations a couple of years back. I started my YouTube channel as one of the ways to keep myself occupied when I retire in the future. Dipping my toes into content creation, getting my feet wet. Ah, some of you might be thinking that my channel is all about investing and personal finance. No! The last thing I ever want to talk about in my retirement years is investing. That phase of my life is over. Sure, I will be monitoring my finances in private, but I am not going to be talking about it on a regular basis, much less make videos about it. Seriously, how many videos can one make about CPF! I want to focus on activities that can be sustained throughout my retirement. Secondly, the topics must not be controversial. I decided on food and traveling. Everyone got to eat right? And I am planning to travel more during my retirement, so might as well create some content while I am at it. Besides, once your portfolio, passive income and CPF reach a certain astronomical amount, it gets kinda pointless talking about it. I would rather spend my time enjoying the fruits of my labour and accumulating more 'Memory Dividends'.

My first ever trip to Tokyo in November was like a practice run and it was amazing. Planning to visit Osaka in 2025! ^^

~ Collecting memories, one destination at a time ~

Total Cumulative Dividends (2010 - 9M2024): S$316, 273

Current Cash & Cash Equivalents (SSB/T-bills): S$42, 000

(*All figures are accurate as of 30 Sep 2024)

Portfolio Actions in 3Q 2024:

Accumulated Sheng Siong at S$1.51

Accumulated Alphabet at US$163

Accumulated Nvidia at US$113

Accumulated Microsoft at US$410

Subscribed to CICT preferential offering with small amount of excess units

My Barbell Approach Continues - 'Sheng Siong + Tech'

The US Federal Reserve finally began the rate cut cycle in September, seeking to normalise interest rates again as inflation trends closer to their 2% target and the US labour market softens. This pivot sent S-REITs sector into an incredible 7-week rally. My REITs-heavy portfolio shot back up to an all-time-high market value of S$784.5k! My total annual dividend income is on track to hit a record-high of S$42k this year, which translates to S$3.5k per month.

Rate cuts provide a tailwind for REITs in three ways. First, as the risk-free rate trends down, the yield spread against REITs would widen. Investors chasing better yields would pile back into REITs, causing prices to rise. For example, if Singapore T-bills yield around 2% next year, then a 5% yield from a blue-chip REIT starts to look attractive. Second, lower interest rates would translate to higher NAV and healthier gearing levels for REITs. Third, DPU could increase as the REITs refinance at lower rates. However, we would only see the effects many quarters later. Honestly, after the relentless rally in September, I think most of the positive sentiments on REITs have been priced in for now.

Surprisingly, the three local banks are still holding up well despite analysts and experts touting that rate cuts are bad for banks. In fact, if we take DBS recent 1-for-10 bonus share issue into consideration, its price is actually more like above S$40. Imagine trading in and out of the market, trying to time the dips and rallies perfectly. I would have missed out on this sudden S-REITs recovery. As a long-term investor, time in the market is better than timing the market. We never know when Mr Market might just make a U-Turn into 'euphoria' mode. By the time we gathered our wits and saw the news on mainstream media, it's probably too late to act.

As for OCBC, its dividend visibility could be boosted if it can gain full ownership of Great Eastern. There is potential for excess capital from Great Eastern to be returned to OCBC shareholders if 100% ownership is successful. Furthermore, compared to DBS and UOB, OCBC has a larger exposure to the Greater Bay Area in China. It stands to benefit from the latest stimulus packages from the Chinese government.

As I have mentioned in my previous portfolio updates, I have stopped accumulating REITs and banks in meaningful amounts since the beginning of 2024. Currently, I am holding more than enough REITs. I am comfortable with the 67% REITs allocation in my portfolio. With the recent run-up in prices, all the more reason I am in no rush to accumulate. More prudent to just sit back, enjoy the rally, collect the dividends and build up some dry powder. The same approach applies to my bank positions. They are at a comfortable 24% allocation level with juicy stable dividends. No compelling reason to accumulate at current lofty valuations. Just hang on tight and surf the wave. Sometimes, doing nothing is the best.

With my core positions remaining intact, most of my buys in Q3 went into US tech companies. My ultimate goal is to hit 10% allocation for 5 tech companies in my portfolio within the next 5 years. These tech positions serve as an avenue for me to reinvest dividends from my income stocks. Even though Nvidia's recent earnings beat market expectations, investors thought the company's forward guidance was not spectacular enough, causing the price to dip sharply in August. I think Nvidia is a victim of its own success, setting the bar too high. The market is more likely to expect crazy growth numbers every quarter. But I am confident of its long-term growth trajectory in the AI sector. Alphabet is embroiled in legal tussle with the US Justice Department. Google is accused of being a monopoly (again!). This is just the usual noise. There is just no realistic alternative to Google Search and Youtube. Took this opportunity to buy the dip. There was a period in August when the market was suddenly fearful of the AI bubble burst, sending Microsoft share price lower. You could say Microsoft suffered some 'collateral damage' post Nvidia earnings. Of course, I added Microsoft during that short period of market fear. Within a week or two, these positions recovered. This shows that we need to have a plan ready and be decisive when the opportunities present themselves, especially in the US market.

(Source: The Straits Times)

(Sheng Siong 5-year dividend track record)

To balance out the volatility of my tech positions, I have been accumulating Sheng Siong shares every quarter since last year. This grocery retail company is a cash-generating machine with a strong balance sheet and sustainable dividend payout. Strong cash-flow and zero debt. This company is like the Costco or Walmart of Singapore. With more rate cuts expected in 2025, Sheng Siong's dividend yield of around 4.2% at $1.50 is starting to look pretty decent. Unlike Banks and REITs, Sheng Siong's earnings is not subjected to interest rate sensitivity.

A secondary reason is that the government has been implementing support measures to help local residents cope with the rising costs of living in Singapore. Although core inflation has slowed down significantly this year, prices remain high. People tend to misunderstand this concept. Slower inflation just means prices are increasing slower, not going lower. In my opinion, the CDC vouchers would probably continue. In fact, each household will receive $300 in January 2025. These vouchers can be spent at supermarkets such as Sheng Siong, thus potentially benefiting the company. Such direct handouts from the government would be difficult to remove as it has proven popular especially among the low-income families and retired elderly. With the costs of eating out rising, more families could choose to cook meals at home more frequently, which also benefits Sheng Siong since most of its stores offer affordable fresh produce too.

Lastly, as we already witnessed during the Covid-19 pandemic, supermarkets' earnings spiked as people were stuck at home during the lockdown period and social-distancing was mandatory. Sheng Siong is practically a pandemic-proof stock. I don't know about you guys, but I assume there is a decent chance of another pandemic in my lifetime. Prudent to be prepared.

BTO Renovation Completed!

Six months after collecting the keys to my HDB BTO flat, renovation works and furnishing is finally completed! I officially moved in last month. Loving that fresh, sweet smell of a new home (with 99-year lease). I went for a modern, minimalist and practical style.

Oh, and Q3 HDB resale prices increased 2.5% QoQ. I have heard plenty of complaints and rants about expensive public housing in Singapore. Let's face it. Property has become just another asset that generates profits and income. It's happening everywhere in developed major cities like Hong Kong, Tokyo, London and New York. Housing is no longer considered a basic human need. Sad, really. But that's the way the capitalistic system is built. No turning back. This system requires a constant stream of home-buyers taking on mortgages from banks. The higher the property prices, the larger the mortgages, the more profits the banks make (more dividends for me >_<). I am just thankful that my flat is fully-paid with my CPF savings. Also glad that I am vested in banks and PropNex. Don't fight the system. Make the most out of it. Find ways to extract benefits from it.

Alright then, time to plan and get ready for my trip to Tokyo in November! ^^

Portfolio XIRR (1H2024): -5.1%(inclusive of dividends)

Dividends Collected (1H2024): S$21, 761 (-2% yoy)

Total Cumulative Dividends (2010 - 1H2024): S$303, 406

Current Cash & Cash Equivalents (SSB/T-bills): S$42, 000

(*All figures are accurate as of 28 Jun 2024)

Portfolio Actions in 1H 2024:

Accumulated more Alphabet at US$137, US$171 and US$178

Accumulated more Amazon at US$176 and US$180

Initiated position in Nvidia at US$124

Accumulated more Sheng Siong at S$1.50 and S$1.52

Accumulated more NetLink Trust at S$0.84

Partial divestment of Apple at US$190

Full divestment of Microsoft at US$409

New Milestone Unlocked - Becoming A Property Owner

My apologies for the lack of updates in 1Q 2024. I was too busy with my BTO flat renovation. Long-time readers of my blog would know that I kickstarted my plan to secure a ‘second pot of gold’ five years ago. The pandemic delayed the construction progress by a year. Finally, I am now a proud owner of a fully-paid HDB flat. My block is just a short 5-minute walk away from the future MRT station, community centre, mall & bus-stop. It is also located within a 1-km radius of four Primary Schools, one of which is the prestigious ACS Pri. In the context of Singapore’s residential property market, it’s a pretty decent location. Resale flats of similar size in the neighbouring estate of Bukit Batok are being transacted at more than double my BTO purchase price. Absolute madness!

DBS The Out-performer

The three local banks delivered a strong set of results in the first half or 2024, especially DBS, which did a bonus share issue with the share price rising even further afterwards. The bank achieved significant growth in private wealth management fee income. The more uncertain the world becomes, the more ultra high-net-worth individuals will seek to park their wealth in a safe haven such as Singapore. We are kinda like the Switzerland of Asia. The banks’ higher dividend payout also helped to mitigate the decline in REITs’ distributions.

DBS CEO Piyush Gupta said, “Our record earnings have given us a strong start to the year. We had broad-based business momentum as loans grew and both fee income and treasury customer sales reached new highs. While geopolitical tensions persist, macroeconomic conditions remain resilient and our franchise is well positioned to capture business opportunities. We are optimistic that total income and earnings will be better than previously guided and we will be able to deliver another year of strong shareholder returns.”

The biggest contributor to DBS's growth is due to Wealth Management. The family office business has seen significant growth, with many high-net-worth individuals and families seeking services for wealth preservation and succession planning. When DBS say they eye S$500 billion in wealth assets by 2026, that is rather conservative. I think the figure should be at least S$750 billion to S$1 trillion. According to Capgemini Research Institute's World Wealth Report 2024, global high-net-worth-individual wealth and population is growing exponentially at 5%.

Building The Pyramid Top

I spent the past 15 years building up my dividend portfolio and CPF savings. Now, with the addition of SSB and a fully-paid property to my asset allocation, I consider the foundation-building phase of my investment journey to be mostly done. Nice timing too. The era of near-zero interest rate and easy monetary policies from the US Fed is likely over. My heavy REIT-accumulation days are over. I already own enough REITs. My current portfolio is already well-positioned for future rate cuts. I already made hay while the Sun was shining. This ties in with my shift towards non-REIT stocks with strong balance sheets, such as US Tech, three local banks & Sheng Siong. Last year, I tried to stick to a ratio of 50:50 with regards to my capital deployment. For example, for every dollar invested in Sheng Siong, another dollar was invested in Apple. Moving forward, I shall tweak the ratio to 20:80. For example, for every $2 dollar invested in DBS, another $8 shall be invested in Alphabet. The bulk of my passive income from REITs shall be channeled towards US Big Tech. Rain or shine, every quarter accumulate. When the market is toppish, buy less. When the market is bearish, buy more. Never all-in. Never use margin.

The peace of mind provided by a fully-paid HDB flat and sizeable CPF savings is priceless. A strong foundation allows me to better stomach the volatility in the US market. Subconsciously, I know I would always have something to fall back on. I just hope the government can continue to grow Singapore’s GDP over the long-term so that my new 99-year lease flat can appreciate in value. :P

Possible Future Landlord

Alright, with the boring concrete strategy out of the way, let’s talk about some possible plans far far into the future. This is just me doing some fun brainstorming and speculation. Perhaps you can call it daydreaming even. Hey, doesn’t hurt to dream a little sometimes, right? Anyway, always prudent to have a Plan B, a viable way to get out of Singapore if there ever is a need to escape the escalating cost of living. Based on my simple research, the average rental rate for a flat of similar size near my neighbourhood is around S$2.5k per month. Let’s be super conservative and assume the rental rate stays the same after 10 years. S$30k per year rental income converted to Malaysian Ringgit or Thai Baht can go a long way in JB or Bangkok. I can live in those cities without compromising my quality of life as a young senior. Both countries are starting to offer more types of retirement Visas. Cheap condo rental. Delicious & cheap local food.

During my trip to Bangkok last November, I observed the food pricing is one level lower than Singapore’s. Their restaurant pricing is similar to our Foodcourt pricing. Their foodcourt pricing is similar to our hawker pricing. And if you are willing to be more adventurous, their street food pricing is lower than anything you can find in Singapore. Their BTS train system is similar to our MRT network. I am planning another longer trip to Bangkok next year! :)

~ Don't Wait To Buy Real Estate. Buy Real Estate & Wait. ~

.png)

.png)

.png)

.png)

.png)